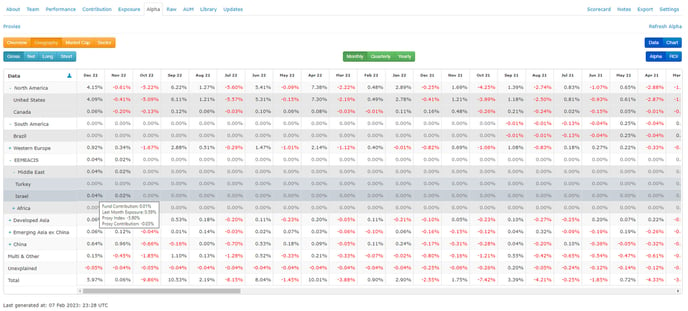

Alpha attribution is calculated using the following equation:

Alpha Attribution = Attribution to Fund - Proxy Attribution

With proxy attribution is calculated using the following equation:

Proxy Attribution = (Last Month Exposure to Fund x Proxy Performance to Fund) x 100

Therefore Alpha is calculated using the following equation:

Alpha = (Annualized performance of the Primary Asset - Annualized Risk-Free Rate - Beta vs Benchmark) × (Annualized Performance of the Benchmark - Annualized Risk-Free Rate)

Alpha is the difference between the primary asset's actual returns and the expected returns based on its beta to the benchmark. Alpha is sometimes interpreted as the value that an investment lead adds over and above the market on a return-adjusted basis.

Within the statistics page, you can view Alpha vs. Benchmark over three years and five years.

Alpha Calculation Example: